The Rise of Buy Now, Pay Later (BNPL) Its Impact on Consumer Finance

The Buy Now, Pay Later paradigm represents a structural shift in how consumer credit is delivered within digital commerce environments.

Executive Summary

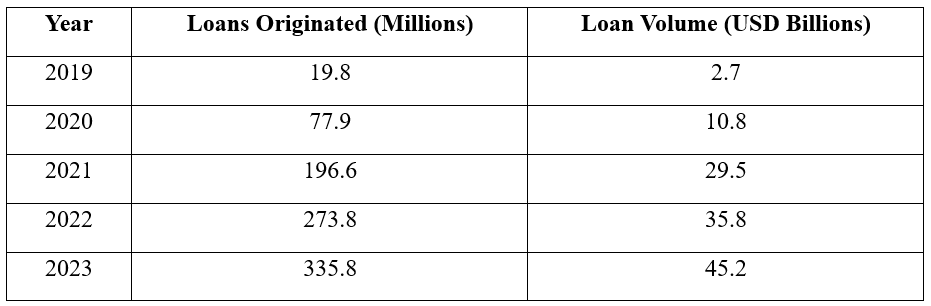

Buy Now, Pay Later (BNPL) has emerged as one of the fastest-growing innovations in digital consumer finance, transforming how short-term credit is delivered at the point of sale. By embedding installment lending directly into online checkout systems, BNPL providers have reduced friction in retail payments while expanding access to short-duration financing. Between 2019 and 2023, BNPL loan originations increased from 19.8 million to 335.8 million transactions, with total lending volume reaching $45.2 billion in the United States alone. This rapid adoption signals a structural shift in payment behavior, particularly among younger consumers who prefer flexible alternatives to traditional credit cards.

Despite its advantages including improved purchasing flexibility and higher retail conversion rates BNPL also raises regulatory concerns related to transparency, consumer indebtedness, and credit oversight. As fintech platforms continue integrating lending into digital commerce environments, BNPL is becoming a central component of embedded finance and an increasingly important area of study for future financial technology professionals.

Introduction

Financial technology continues to redefine the structure of modern payment systems by integrating credit services directly into digital platforms. One of the most influential developments within this transformation is the rise of Buy Now, Pay Later (BNPL), a short-term installment financing model that allows consumers to make purchases immediately while spreading payments over time. Unlike traditional credit cards, BNPL services typically operate through simplified approval processes and are embedded directly within online checkout environments, making access to credit faster and more intuitive.

The expansion of BNPL services closely follows the growth of global e-commerce and changing consumer expectations regarding payment flexibility. Regulatory evidence shows that BNPL loan originations increased from 19.8 million transactions in 2019 to 335.8 million in 2023, while total lending volume rose from $2.7 billion to $45.2 billion during the same period. These trends highlight the increasing role of installment-based financing within everyday retail transactions (Federal Reserve, 2025).

Understanding the BNPL Model

BNPL is a short-term installment lending mechanism that allows consumers to divide purchases into smaller payments over several weeks or months. Most BNPL arrangements follow a “pay-in-four” structure, where consumers make an initial down payment followed by three additional installments at fixed intervals.

The core BNPL lending interaction involves three primary participants:

the consumer

the merchant

the BNPL provider

Once a consumer selects BNPL at checkout, the provider pays the merchant immediately while collecting repayments from the consumer over time. This structure benefits retailers through guaranteed upfront payment while improving purchasing flexibility for customers.

Unlike traditional lending systems that rely heavily on credit history evaluation, BNPL providers frequently use automated digital risk-assessment tools. This allows approvals to occur within seconds, demonstrating how fintech platforms are embedding credit directly into commerce environments.

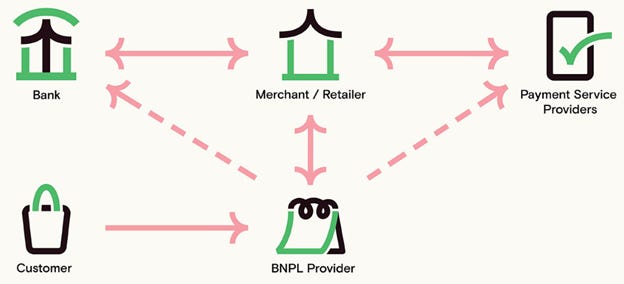

BNPL Transaction Ecosystem

Figure 1 illustrates the Buy Now, Pay Later transaction ecosystem, highlighting the interaction between customers, merchants, BNPL providers, banks, and payment service providers within a digitally embedded credit infrastructure.

In this ecosystem, the BNPL provider acts as the intermediary lender that pays the merchant at the point of purchase while collecting installment repayments from the customer over time. The merchant benefits from immediate payment confirmation and reduced checkout friction, while consumers gain access to short-term financing embedded directly within the purchasing process.

Banks play a supporting role by providing settlement accounts, liquidity infrastructure, and regulatory compliance frameworks that enable BNPL providers to operate within established financial systems. In many cases, partner banks also assist with underwriting support and transaction authorization across card networks.

Payment service providers facilitate communication between merchants and BNPL platforms by enabling checkout integration, transaction routing, and authorization processing within digital payment environments. These providers ensure that installment payment selections can be executed seamlessly during online transactions.

Within the BNPL ecosystem diagram, solid arrows represent direct financial payment flows between participants, while dashed arrows represent supporting infrastructure relationships such as settlement processing, authorization routing, and platform integration services performed by banks and payment service providers.

Growth of the BNPL Market

BNPL adoption has accelerated rapidly over the past five years, reflecting broader shifts in consumer payment preferences and digital retail expansion. Regulatory data show that BNPL lending volume grew dramatically between 2019 and 2023.

This growth reflects increasing integration of installment financing into digital retail platforms. In 2023 alone, approximately 53.6 million consumers used BNPL services, representing a 12% increase from the previous year (Federal Reserve, 2025).

Additionally, usage intensity is rising. The average number of BNPL loans per consumer increased from 5.7 loans in 2022 to 6.3 loans in 2023, while annual borrowing per user rose from $745 to $848. These figures indicate that BNPL is evolving from an occasional payment tool into a recurring financing method.

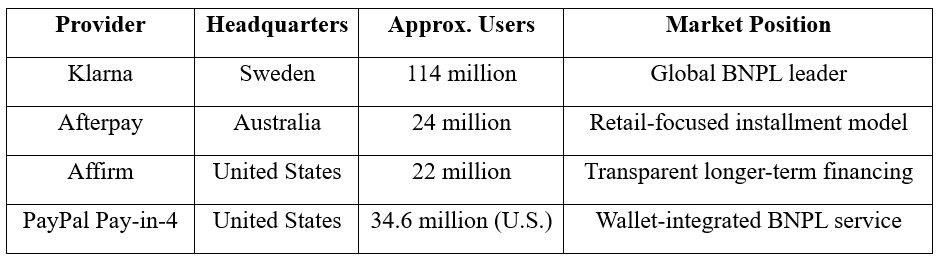

Major BNPL Providers

The expansion of the BNPL ecosystem has been driven primarily by fintech firms embedding installment lending into online retail platforms. Leading providers include Klarna, Afterpay, Affirm, and PayPal.

These firms illustrate how fintech platforms are reshaping credit delivery by embedding financing directly into checkout systems.

Benefits of BNPL

BNPL services provide several advantages for consumers and merchants within digital commerce ecosystems.

First, BNPL improves purchasing flexibility by allowing consumers to spread costs across multiple payments without incurring interest when repayments are made on time.

Second, retailers benefit from higher conversion rates and increased order values. Industry payment research shows installment payment options reduce checkout abandonment and encourage larger purchases (Worldpay, 2024).

Third, BNPL expands financial access for consumers with limited credit histories. Because approvals often rely on alternative risk-assessment methods rather than traditional credit scoring systems, BNPL can support broader participation in digital commerce.

Finally, usage data indicate growing consumer engagement with installment financing. The average number of BNPL loans per user increased by 11% between 2022 and 2023, demonstrating increasing reliance on flexible payment structures (Federal Reserve, 2025).

Risks and Challenges

Despite its advantages, BNPL introduces several financial and regulatory concerns.

One major risk involves overextension of short-term borrowing. The convenience of instant approval can encourage repeated borrowing across multiple providers, increasing the likelihood of repayment stress.

Regulatory data indicate that 4.1% of BNPL loans incurred late fees in 2023, highlighting potential repayment challenges among some users (Federal Reserve, 2025).

Another concern involves transparency. Unlike traditional credit products, BNPL agreements are sometimes perceived as payment tools rather than borrowing arrangements, which may reduce consumer awareness of financial obligations.

Although default rates remain relatively low with charge-off rates declining to 1.83% in 2023 continued market expansion increases the importance of monitoring credit risk exposure (Federal Reserve, 2025).

Future of BNPL in FinTech

BNPL is expected to play an increasingly important role within the broader embedded finance ecosystem. As fintech platforms integrate lending services directly into digital marketplaces, installment financing is likely to become a standard checkout feature rather than a niche payment option.

Future developments may include:

integration with digital wallets

expansion into subscription commerce

use of AI-driven credit risk assessment

stronger regulatory oversight frameworks

As competition intensifies, providers are also diversifying beyond short-term installment lending into longer-duration financing products and hybrid credit solutions.

Conclusion

BNPL represents a structural shift in how consumer credit is delivered within digital commerce environments. Rapid growth in loan originations, increasing user adoption, and deeper integration with online retail platforms demonstrate that installment-based financing is becoming a permanent component of modern payment systems.

While the model improves purchasing flexibility and expands financial access, it also introduces new regulatory and behavioral challenges that require careful oversight. For fintech professionals and students, BNPL provides a valuable case study in how technology is transforming credit delivery, reshaping consumer behavior, and redefining the boundaries between payments and lending in the evolving financial ecosystem.

References

Worldpay. (2024). Global Payments Report 2024. https://www.worldpay.com/global-payments-report

Board of Governors of the Federal Reserve System. (2025). Economic Well-Being of U.S. Households in 2024. https://www.federalreserve.gov/publications/files/2024-report-economic-well-being-us-households-202505.pdf

Consumer Financial Protection Bureau (CFPB). (2023). The Consumer Credit Card Market Report. https://files.consumerfinance.gov/f/documents/cfpb_consumer-credit-card-market-report_2023.pdf

Consumer Financial Protection Bureau (CFPB). (2023). Consumer Use of Buy Now, Pay Later.

https://files.consumerfinance.gov/f/documents/cfpb_consumer-use-of-buy-now-pay-later_2023-03.pdf

Bank for International Settlements (BIS). (2023). Buy Now, Pay Later: A Cross-Country Analysis. https://www.bis.org/publ/qtrpdf/r_qt2309x.htm